what a company should do to improve its roe

As a stock market investor, y'all will always be on the sentry for companies that consistently earn high profits and accept the ability to do it using their existing resources. To identify the right candidate investors often rely on the return on equity (RoE) metric — the management'southward efficient employ of investors' funds to generate earnings growth. While this metric is very useful in almost cases, information technology does not always reveal a company's limitations and the risks fastened to information technology. Therefore, information technology becomes imperative to dig a bit deeper and detect out from where the visitor is deriving its profits.

Deconstructing RoE

RoE is a good starting betoken to zero in on financially sound and profitable businesses. Information technology is arrived at by dividing the company's profit after taxation (PAT) by the total shareholder equity. The higher the company'southward RoE, the amend it is at employing investors' capital to generate profits. Ascension in RoE shows that the company is able to generate profits without adding new disinterestedness into the business. High-growth companies typically take a higher RoE. Analysing the tendency in terms of a company's ROE and comparing it to industry peers can prove where the company stands.

Yet, a high RoE may non reveal the consummate story about the company'south operations. For case, a company may showroom a strong RoE merely by taking on huge debt on its books. Funding growth through borrowings leads to high interest expenditure, which, in turn, reduces profitability in the long run. It may also somewhen lead the company to defalcation. RoE can also exist high if the visitor has diluted its equity by selling more shares. Doing so lowers its earnings per share by increasing the number of outstanding shares.

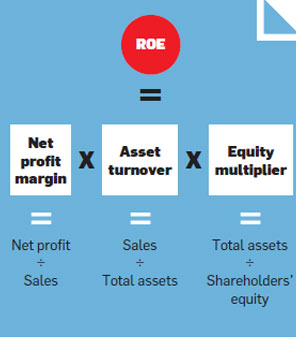

Given these limitations, it is necessary to identify heads that are actually driving the returns. The Du Pont model helps deconstruct the RoE metric into distinct parts, showing exactly how the company is achieving its ROE — whether information technology is through increasing profit margins, higher asset turnover or employ of leverage. Nether the three-step model of the Du Pont analysis, RoE is calculated as follows:

The iii-step DuPont model captures the efficacy of the company direction to generate profits (net profit margin), utilise its assets (asset turnover) and deploy optimal leverage (equity multiplier). Ideally, investors would desire to put money in a company which is generating the RoE by increasing its net turn a profit margin or its asset turnover, or both. The internet profit margin shows how much earnings the visitor generates from each rupee of sales. A higher or increasing profit margin suggests its pricing power and competitive advantages over its peers. Asset turnover of the visitor measures how much sales information technology generates from each rupee of avails. Generating more sales on less assets implies that the visitor is non required to invest more funds to purchase assets in an attempt to generate revenues. Information technology essentially indicates the management'south efficiency in utilising its existing assets to drive sales.

But, if equity multiplier is the but criterion to boost the company's ROE, information technology could be a worrying sign, every bit it implies the apply of financial leverage to generate returns. If a company already has high leverage, taking on additional debt may increment the risk of default and chances of going broke. However, e'er think it is likewise important to compare the RoE and other financial ratios of other companies engaged in similar business organisation because each industry operates under unique constraints. For example, yous cannot realistically compare RoEs of a FMCG visitor, such equally Hindustan Unilever, with that of a banking company such as HDFC Bank. By the very nature of its business, HDFC Bank is required to apply financial leverage to drive returns, whereas HUL requires hardly any borrowings, as information technology is a high cash period generating business organisation. Similarly, net profit margins and asset turnover levels also vary from manufacture to industry.

Functioning of industry majors

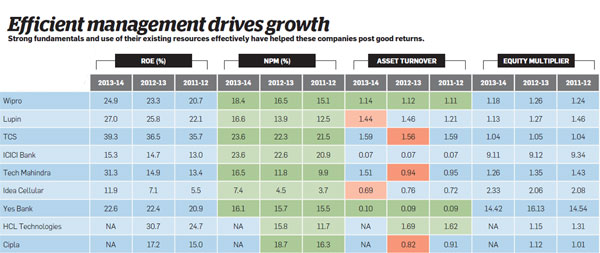

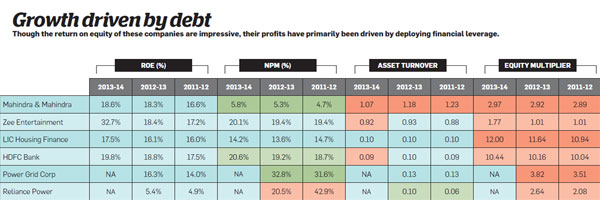

For your benefit, nosotros have analysed the financials of the superlative 100 companies listed on the BSE to encounter how they are generating their RoE. Data shows only 16 companies from the BSE 100 universe have exhibited consistent improvement in RoE over the past three years. However, farther assay of the RoE shows that six of these companies take also exhibited a sustained increment in their equity multiplier. Two of these — HDFC Bank and LIC Housing Finance — are in the financial services industry which works purely on leverage, so they can be forgiven for it. Besides, they have also shown improvement in either profit margin or asset turnover.

This reflects the efficiency of the direction of these companies. Just others exercise not fare well on these counts. Public sector power utility Power Grid Corporation has fabricated use of leverage to generate the rise in its RoE over these years, but has too simultaneously shown improvement in net profit margin as well as its asset turnover. However, a closer look reveals that the biggest driver of the ROE growth for Power Grid has been an increase in its disinterestedness multiplier.

NA- Not available, RoE - Return on Equity, NPM - Net Profit Margin Dark-green boxes announce positive change in parameter while reddish boxes show negative change in parameter compared to the previous twelvemonth. Source: ETIG Database

While Reliance Power has also used leverage to heave its RoE at 5% information technology has nevertheless not been able to evangelize higher render than its cost of equity to its shareholders. Mahindra & Mahindra has succeeded in improving RoE to 19%, but by and large on of 33%, Zee Entertainment may look similar a fundamentally strong company, but its increasing leverage coupled with near-stagnant profit margins and asset turnover suggests that the visitor is not using resource efficiently. Zee is the most vivid case of why it is of import to analyse the components of RoE. Had we relied purely on the RoE metric, it would have led us to believe that Zee is in a much stronger position than it actually is.

There are ten companies showing sustained improvement in RoE either on the dorsum of operational efficiency or asset turnover, without adding to their leverage. Of these, Tata Power does non authorize every bit a practiced candidate every bit its RoE is low compared to some of its manufacture peers. The first visual is a snapshot of the nine companies that are showing sustained comeback in RoE over the last three years across all parameters under consideration.

NA- Non available, RoE - Return on Disinterestedness, NPM - Net Profit Margin Green boxes denote positive alter in parameter while red boxes show negative change in parameter compared to the previous year. Source: ETIG Database

Pharma major Lupin has seen its RoE climb over the last three years from 22.1% in 2011-12 to 27% in 2013-fourteen. Examining Lupin's threestep DuPont calculations, shows that the company has managed to improve its net margin from 12.5% to 16.6% during the period, while increasing its asset turnover from ane.21 to 1.44. Its equity multiplier has continuously declined over the menstruation under consideration, clearly showing the former metrics are behind the high RoE. Another pharma company Cipla has delivered robust shareholder return over the by few years, with the RoE jumping from xiv.five% in 2010-11 to 17.ii% in 2012-xiii (2013-14 data is not declared yet). While Cipla's asset turnover, or sales generated per rupee of assets, is quite low equally compared to Lupin. It enjoys much higher profit margins and this has resulted in the ascent in its RoE.

Tata Consultancy Services, the land's largest visitor by market capitalisation, also ranks loftier in terms of management efficiency. The software giant'due south RoE has increased from 35.seven% in 2011-12 to 39.3% in 2013-14, along with a jump in profit margin from 21.five% to a healthy 23.half-dozen%. A depression disinterestedness multiplier indicates that the visitor relies more than on turn a profit margin to generate returns for its shareholders. HCL Technologies, a smaller rival to TCS, ticks all the check-boxes when it comes to efficiency. Its RoE has expanded from 21.v% in 2010-11 to xxx.seven% in 2012-thirteen according to latest data available. It enjoys the highest nugget turnover amid its peers, which has contributed to its returns apart from a rise internet profit margin. Wipro also comes up trumps on all parameters, even so enjoys a lower RoE than nearly of its industry peers.

While its net profit margins are college than Tech Mahindra and HCL Technologies, information technology generates much lower revenues for every rupee of avails as compared to its rivals. The Azim Premji-founded business firm has been reporting poor gear up of numbers for a while at present even every bit its rivals have washed far amend. Another Information technology company, Tech Mahindra, has exhibited strong RoE growth over the past three years. Like its larger rival TCS, the primary commuter backside the improving returns is the visitor'south operational efficiency. Its internet profit margin has jumped from 9.9% in 2011-12 to xvi.5% in 2013-14. Its takeover of scandal-hit Satyam has helped information technology reap the do good of scale and cross-selling opportunities.

ICICI Banking company'due south RoE has jumped from 13% in 2011-12 to 15.3% in 2013-fourteen. Just, has its high disinterestedness multiplier helped information technology boost returns? No. Its leverage has actually gone down during this period. Bulk of its RoE has been generated by its operational efficiency, equally indicated by the net profit margin. The bank's NPM stands at 23.6% at the end of terminal financial year compared to twenty.9% three years ago. Yes Bank besides employs very high leverage, but that is not the reason for its increasing RoE. Similar ICICI Bank, Yep Bank'due south cyberspace profit margin is contributing to its returns, having increased from 15.five% in 2011-12 to 16.1% at the end of 2013-14.

Among telecom companies, Idea Cellular is clearly the most efficient in the operations front end. At 11.ix%, its RoE is about three times more compared to its rivals Bharti Airtel and Reliance Communications. It not but fetches more revenues for every rupee of its avails, just has also shown improvement in turn a profit margins compared to its peers. Despite a connected rise in use of leverage, both Bharti and Reliance Communications have seen their RoE fall over the by three years. account of increasing leverage. Its net profit margin is also showing a sustained increase, but is still very low at 6%.

Source: https://m.economictimes.com/markets/stocks/news/deconstructing-roe-improving-efficiency-an-important-parameter-while-investing-in-companies/articleshow/39474563.cms

0 Response to "what a company should do to improve its roe"

Post a Comment